Business Asset Disposal Relief (BADR)—previously known as Entrepreneurs’ Relief—is a tax break that reduces the rate of Capital Gains Tax (CGT) when you sell or close a business. It’s designed for directors and business owners who are stepping away from a company they’ve built up significant cash reserves in.

If your company qualifies, BADR lets you pay 14% CGT on the gain instead of the usual CGT rate. The BADR rate will rise to 18% from April 2026, so acting before then could mean a lower tax bill.

What happened to Entrepreneurs’ Relief?

Entrepreneurs’ Relief was rebranded as Business Asset Disposal Relief in 2020, when the lifetime limit was also reduced from £10 million to £1 million. The aim of the relief stayed the same: to reward business owners by reducing tax when they dispose of their company or shares.

Many people still use the term “Entrepreneurs’ Relief” today, which is why you’ll often see both titles used together.

How does Business Asset Disposal Relief work?

You can usually claim Business Asset Disposal Relief when you close your cash-rich company using a Members’ Voluntary Liquidation (MVL). This is a formal process for closing down a solvent company.

If your company has over £25,000 in retained profits, using an MVL usually makes the most financial sense. That’s because distributions made through an MVL are treated as capital rather than income. And if you qualify for BADR, the first £1 million of qualifying gain is taxed at just 14%.

MVL is often used by directors who are retiring or changing careers, have completed a one-off project and no longer need the company, or are restructuring a group of companies.

This is how it might work in a real-life scenario…

- Your company has £100,000 in retained profits

- You liquidate it via an MVL

- After costs, you receive £95,000

- You qualify for BADR, so you pay £13,300 in tax (14%) instead of CGT, as you would if it were treated as income

The larger the retained profits, the more tax you could save. That’s why MVLs are often used by directors of cash-rich companies. That means the company has no debts and significant reserves sitting in the bank.

Who qualifies for Business Asset Disposal Relief?

To qualify for BADR, you need to meet the following criteria:

- You’re an employee or officer of the company (e.g. a director)

- You own at least 5% of the shares and have voting rights

- The company is a trading business, not an investment vehicle

- You’ve met these conditions for at least two years before the disposal

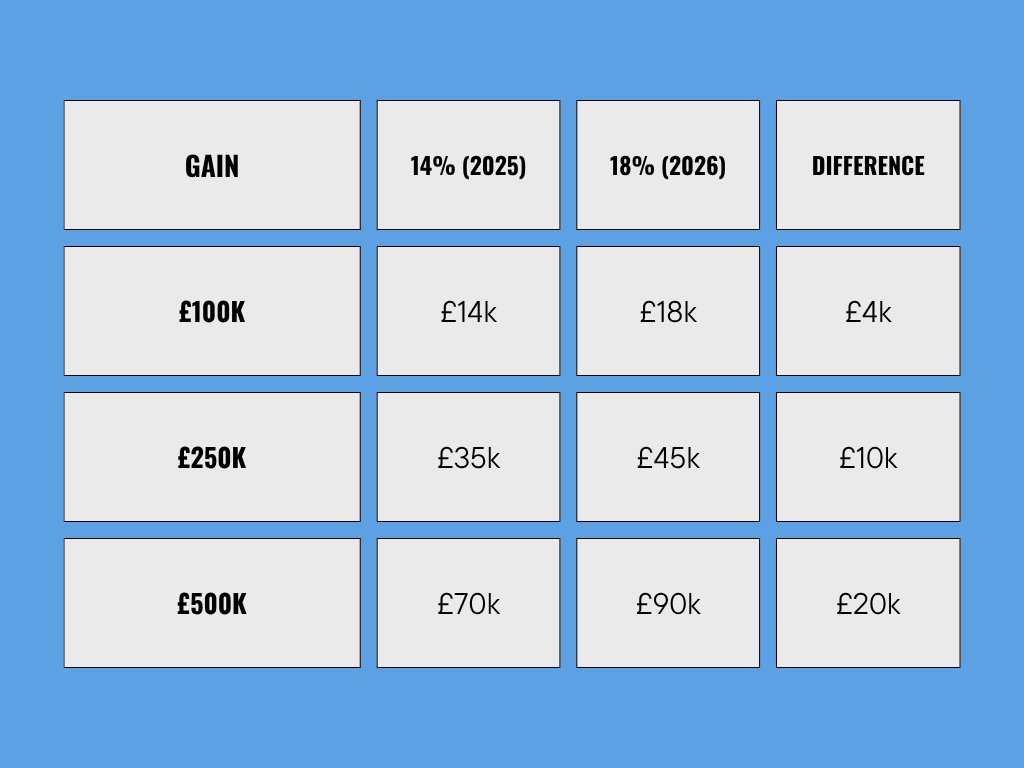

Why act before April 2026?

From April 2026, the BADR rate rises to 18%. That’s an extra £40,000 in tax on a £1 million gain. If you’re planning to close a company with significant retained profits, that difference matters.

Here’s how it compares:

If you’re thinking about liquidating, it may be worth accelerating your timeline to take advantage of the lower rate.

Is an MVL worth it financially if I have less than £25k?

If you’ve already submitted a DS01 and realise your company has outstanding debts, it’s important to act Below the £25,000 mark, the financial benefits of an MVL start to disappear. That’s because if you strike off a company with less than £25k in retained profits, HMRC allows those funds to be treated as capital, without needing to go through a formal liquidation.

Above that threshold, however, an MVL becomes essential if you want to qualify for CGT treatment and access Business Asset Disposal Relief. So while BADR technically applies to any size gain, it’s only practical to pursue if you’re extracting more than £25,000.

Does my company need to be trading?

Yes, if you’re relying on Business Asset Disposal Relief. HMRC specifies that the company must be a “trading company” or a holding company of a trading group. That means most of its activity must involve providing goods or services, rather than holding investments.

If your company has become largely dormant or has significant investment activity (like property or stocks), you may not qualify. A licensed insolvency practitioner will oversee the whole process and so give you advice on whether to proceed or not, before you commit to anything.

Business Asset Disposal Relief and insolvency

Business Asset Disposal Relief is only available when closing a solvent company through an MVL. If your business is in financial difficulty, owes money to creditors or can’t pay its tax liabilities, you won’t be able to use BADR. You’d instead be looking at a Creditors’ Voluntary Liquidation (CVL), where different rules apply and tax benefits like BADR are not available.

Is Business Asset Disposal Relief right for you?

If you’ve got retained profits of £25k or more and are ready to close the company, a Members’ Voluntary Liquidation could be the most tax-efficient way to do it, so you can claim Business Asset Disposal Relief. But remember that BADR is not automatic. Your company must be solvent, you must meet the conditions, and the timing has to be right.

If you’re unsure whether your company qualifies, or whether an MVL is worth it, get in touch. We’ll give you a straight answer and help you plan your next step.