If your company is closing and you’re expecting a payout, it’s important to understand how that money will be taxed. Depending on how your company is closed, distributions can be treated very differently by HMRC.

What is a liquidation distribution?

A liquidation distribution is the money or assets paid out to shareholders after a company has settled its debts and completed the liquidation process. This is when it usually happens:

- In a Members’ Voluntary Liquidation (MVL) when the company is solvent

- Very rarely in a Creditors’ Voluntary Liquidation (CVL), if any surplus remains after paying creditors

The way these distributions are taxed depends on the financial position of the company and your role as a shareholder.

How are distributions taxed in an MVL?

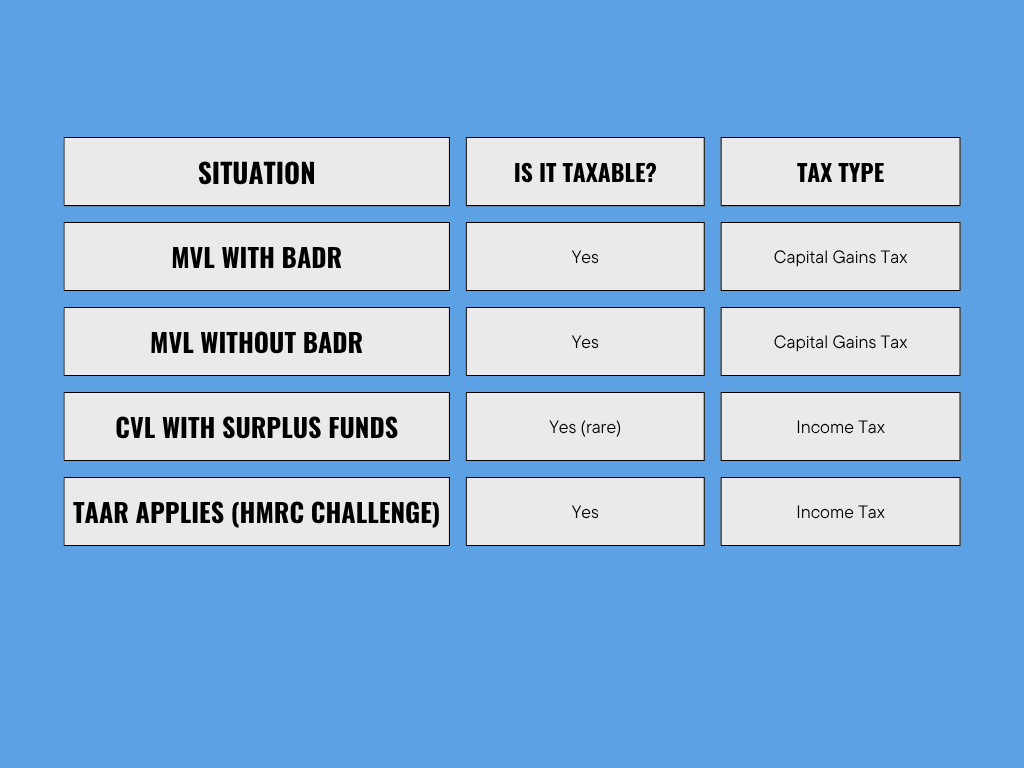

If you’re closing a solvent company using an Members’ Voluntary Liquidation, any money paid out to shareholders is treated as a capital distribution, not income. This is good news, because:

- You’ll pay Capital Gains Tax (CGT) instead of Income Tax

- If you qualify for Business Asset Disposal Relief (BADR), the CGT rate could be just 10%

To qualify for BADR, you need to:

- Own at least 5% of the company’s shares

- Be an employee or director

- Have held the shares for at least two years

If you tick those boxes, distributions up to a £1 million lifetime limit can attract the lower rate, which is traditionally lower than dividend tax. This is why many directors choose MVL when closing a profitable company. It’s a tax-efficient exit strategy.le the process, so they should ensure the timeline and documentation support your deductions.

The CGT rate is rising

The current Business Asset Disposal Relief rate is 14%, but it’s due to rise to 18% from April 2026. That might not sound like much—but if you’re extracting a six-figure sum, the difference could be thousands in extra tax. Acting now could secure the lower rate and maximise your return.

Thinking of closing your company before the tax rate goes up? Now’s the time to act. Get in touch for free, confidential advice and we’ll talk you through how to lock in the current rate.

How are distributions taxed in a CVL?

In a Creditors’ Voluntary Liquidation (CVL), the company is insolvent. That means there are usually no distributions to shareholders because all available funds go to paying creditors.

If, in a rare situation, there’s a small surplus left after creditors are paid, then it may be distributed to shareholders. In this case, the distribution is typically taxed as income, especially if it’s treated as a dividend or is not part of a capital return.

Because distributions from CVLs are almost unheard of, most directors won’t need to worry about personal tax implications here, unless they’ve taken money from the company before liquidation, which could cause issues (especially with HMRC).

The TAAR: HMRC’s anti-avoidance rule

If you’re using an MVL and planning to set up a new company shortly after, you need to be aware of the Targeted Anti-Avoidance Rule (TAAR). HMRC may treat your liquidation distribution as income instead of capital gains if:

- you set up a similar business within two years

- the purpose of the MVL was to reduce your tax bill, or

- you plan to continue the same trade through a different company

This could result in a much higher tax bill. Instead of CGT the lower rate, you could be hit with income tax at up to 45%. If you’re planning to start again under a new name or structure, we can give you the advice you need before moving forward.

An overview of when are distributions taxable

Want to close your company tax-efficiently?

Understanding how liquidation distributions are taxed can help you plan smarter, keep more of your final payout, and avoid HMRC disputes.

If you’re unsure how your distribution will be treated—or worried about triggering TAAR—take advice before proceeding.

Speak to one of our licensed insolvency practitioners today for free, confidential advice tailored to your situation.